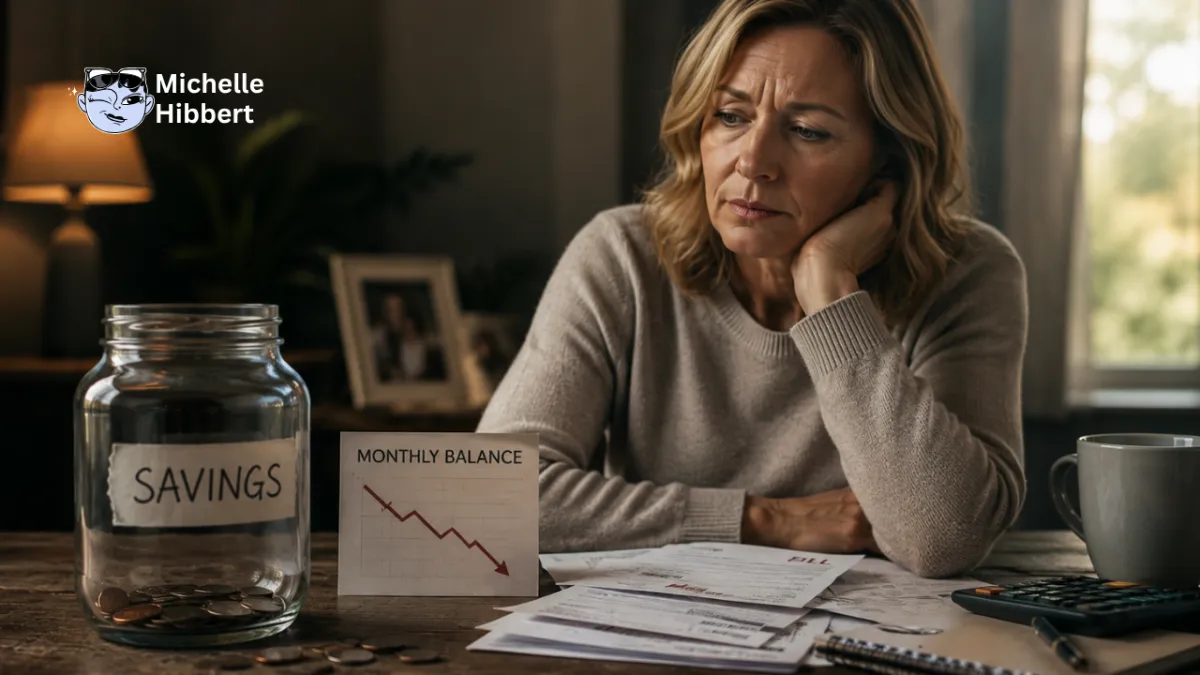

Your savings are shrinking. Your adult child doesn't see it.

Last month, a mother told me she was paying her 26-year-old son's phone bill, car insurance, and helping with rent. None of it bothered her individually. What bothered her was realizing she had no idea when any of it would end.

There was no agreement. No timeline. No conversation about what came next.

That's the part that costs families the most.

Not the amount. The absence of a plan.

There's a version of financial support that makes complete sense. Helping with a deposit. Covering a phone bill while they find their feet. A few months of breathing room while the first job gets sorted.

But that's not the problem.

The problem is when the breathing room turns into year two. When the phone bill is still yours at 25. When the transfers have become so routine that stopping them would feel like pulling the rug so you don't stop. You just quietly adjust your own life around them.

Most parents don't notice the moment it shifts. They're too busy trying to help.

Here's what nobody tells you about launching adult children: the financial part doesn't sort itself out. It has to be planned. And the plan has to be said out loud — to yourself, and to them.

Here's how to build one.

Step 1: Write down everything you're currently covering.

All of it. Phone. Car insurance. Subscriptions. The $50 that appears when things get tight. The grocery run you did "just this once" three months ago that is now quietly monthly.

Add it up.

Not to feel bad about it but to see it clearly. Most parents have never looked at the actual number and the number, when you finally see it, has a way of making the conversation feel a lot more necessary.

Step 2: Decide what stays, what goes, and when.

Some of what you're covering is fine to continue for now. The issue is never the support itself. It's the missing end date.

Every item on that list needs one. Not "when they're more stable" a real date, or a clear milestone. "I'll cover your insurance until March. After that it moves to you." That's a plan. "We'll figure it out as we go" is how you end up here in the first place.

Step 3: Have the conversation before the crisis hits.

This is the one most families skip.

They wait until the money is genuinely tight, or until resentment has been quietly building for months, or until the adult child does something that makes the parent finally snap. And then the conversation happens but under pressure, with emotion attached, and with no structure underneath it.

The conversation you have in advance is a completely different one.

Do it when things are calm. Tell your adult child what you're covering, what you're stopping, and when. Not as a threat but as information. They deserve to plan around reality, not around the assumption that you're fine.

Because here's the thing you've been telling them you're fine.

Step 4: Phase it out. Don't cut it off.

A hard stop at an arbitrary date helps nobody. A phased withdrawal does.

Month one, you cover X. Month three, they take over Y. By month six, the last item was transferred. This gives your adult child time to build the income and habits that make independence actually sustainable. Plus it gives you a clear picture of what you're committing to so there's no quiet extension because it didn't feel like the right moment.

The right moment is always going to feel slightly uncomfortable. That's not a sign to wait. That's just what this transition feels like.

Step 5: Separate emergency support from ongoing support.

These are two different things and they need two different conversations.

If something goes wrong at 11pm on a Tuesday, of course you're going to help. Nobody is suggesting otherwise.

The plan is about the recurring, expected, normalised costs, the ones that have quietly become part of your monthly outgoings without ever being agreed upon. That's what needs the structure. The emergencies take care of themselves. The routine is what erodes savings slowly and without anyone noticing.

Step 6: Review it together. Out loud.

A plan that gets made once and never revisited quietly expires.

Set a date three months in, six months in. Sit down together and ask honestly: is this working? Are they building the skills they need? Or are the supports still in place because it's easier than having the follow-up conversation?

Reviewing the plan is not a sign of distrust. It's what adults do when they're trying to get something right together.

Most parents aren't funding their adult child out of weakness. They're doing it out of love and out of the absence of any other plan.

But love without structure isn't kindness it's expensive and unclear for everyone involved, including the adult child who is trying to build a life on the ground that keeps shifting.

One is support. The other is substitution.

Your savings shrinking quietly in the background while nothing gets said that's not the ending anyone planned for. It's just what happens when the plan never existed.

You don't need to cut your adult child off. You need a conversation and a structure that means your support actually lands the way you intended it to.

That's exactly how I can assist parents with their emerging adult. I get them off parents payroll gradually and systematically.

If this is sounding familiar, the transfers with no end date, the number you haven't added up yet, the conversation you haven't quite had, let's talk.

One call is usually enough to get clear.

→ Book a call here: Link